The last article asked if public works projects really have to take this long. This article asks if P3s are the right answer to the funding crisis.

|

| The Washington suburb Purple light rail line is a 100% P3 project |

In other words: Build now, pay later, but pay more, lots more. A P3 project doesn't mean the private sector contributes or funds a project, it means the private sector finances a project! The cost to the public is simply deferred to a future point. Cost plus interest plus profit. In the case of the Purple Line a $2 billion project balloons to $5.6 billion for total cost. So if the public sector doesn't have the money to pay for a project and not enough credit to get it financed the conventional way, through bonds, for example, than a P3 can mortgage the future even more than a simple bonds issue would do it.

The irony in the Maryland transit case is, that the then Governor had done everything to shore the public funds up through gas tax increases that would pay for the projects. But when the cost projections outpaced the revenue projections, private public partnership was rolled on stage and one of the projects was declared a P3. When the other was still too expensive half of it was also declared P3, an especially "creative approach": half bid the conventional way with a fully designed set of plans and specs, the other half offered to the private sector to be designed and built out of one hand. Is P3 a potentially Trojan horse?

|

| Are P3s really necessary to close the infrastructure gap? |

When a new Governor was elected in Maryland he killed the hybrid model transit project and left only the full P3 project to survive (its actual survival is still a question). This way nobody could find out whether the hybrid model would have produced two compatible halfs. When the state made these P3 decisions, it had only two P3 projects under its belt, neither was transit. The two previous Maryland public private partnerships were a major investment into the Port of Baltimore and two State owned travel plazas on I-95. In both cases the state maintained ownership of land and facilities and leased them out to a private entity which operates them for a set period of time.

P3 for transit is still relatively new in the US and there a only a few North American precedents, the first was the Hudson Bergen rail line in New Jersey and a recent prominent project is the Eagle rail line to Denver's airport. The Purple Line and these two P3 transit projects happen to all cost about $2 billion to construct.

|

| Payback from user fees: Toll Roads |

The industry sees a great future for P3. American Investment Group (AIG) pronounces in a brochure titled The United States: The World’s Largest Emerging P3 Market:

After decades of underinvestment and an increasing population, today’s infrastructure needs are large and continue to grow. Federal, state and local governments are finding it difficult to finance new projects on their own due to decreased tax revenue and shrinking budgets. These two factors have increased the political will and desire to seek alternatives to the traditional “design-bid-build” procurement methodology. Many states and the federal government agree the P3 model maximizes value for their constituents, delivers a lower total cost, and can be delivered quicker. (AIG)In fact, the entire P3 market in 2012 was smaller in the US than in Canada, even though Canada's economy is only about a tenth of the US economy. This is rapidly changing with the US warming to private sector public works involvement just when Europeans are beginning to draw back from it to some extent.

The idea that P3s allow infrastructure to be built for free is economic snake oil. If P3s are structured so that no funds come from tax revenues, then this simply means that tolls or some other user fee are the funding mechanism. User fees can be an economically efficient way to pay for infrastructure, but they do not require that a private partner be involved; governments can fund infrastructure with user fees while financing the project with traditional tax-exempt municipal bonds. In other words, while tolls and user fees are not taxes per se, they are still a cost that must be borne. (Hunter Blair, No Free Bridge)

In the case of the 100% P3 Purple Line deal, the private consortium dubbed the Purple Line Transit Partners will finance $1 billion of the roughly $2 billion construction cost and build the project over six years. In turn it receives a 30-year right to operate and maintain the line and receive a set annual fee of $150 million. State, federal and local funds pay $990 million of the construction costs.

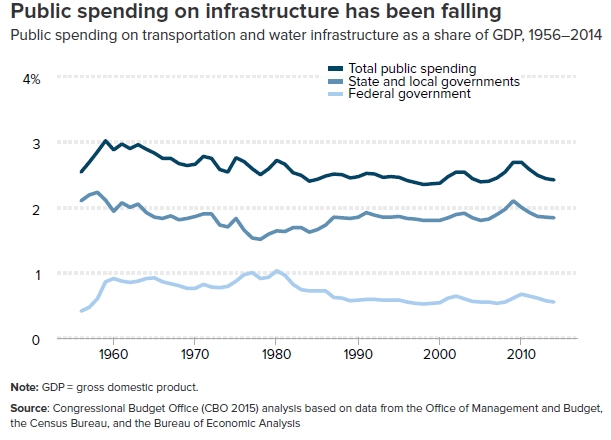

sinking infrastructure investments in relation to the GDP

Even a rather optimistic ridership forecast of 59,500 daily passengers will not be able to fund the obligations for at least 15 years. Maryland's DOT envisions to cover the shortfall with fares from the MARC commuter trains also run by DOT which have the best cost recovery rate among Maryland's transit modes. The total cost for taxpayers: $5.6 billion (including the operating costs over 30 years). It isn't easy to see if this is a good deal or not and the lawmakers and approval bodies had a hard time working through the 800 plus page contract in the 30 days they had for review.

The contracting team will mostly be responsible for keeping the construction cost and schedule (a big deal in any large project) but the public side carries the risk for ridership. The construction cost bid was about 1/2 billion less than the final estimates by the State funded original design team which had prepared the bid package including design-build performance specifications and preliminary design drawings and had completed the required environmental and New Starts studies. This significantly lower cost is suspicious. With construction cost "low balled" to win the bid contractors often assume they can find ways to recover the cost through "change orders", a method considerably easier to employ in a traditional design-bid-build process than in a design-build where much more responsibility for final construction documents and cost management rests with the contractor.

One assumption of P3 proponents is that the private sector cannot only procure services cheaper but can also construct more efficiently than the public sector, in part because design and construction are in one hand, and in part because the private sector is less restrained by rules and regulations. The latter mostly means lower wage rates (not paying Davis Bacon wages, for example), not really an efficiency indicator.

That "logic" of private efficiency is then sometimes taken even further to operations and management, assuming similar efficiencies there. Design-build projects in which the private side bids for integrated design and construction are thus expanded to operations (Design, build operate) and potentially management. (DBOM). The 17 year old Hudson Bergen Line was such a project.

|

| Purple Line cost and funding graphic (Washington Post) |

A 2007 study of Australian PPP projects found some significant differences in on-time and under-budget performance between design-build and the traditional design-bid-build. It found an 8% difference in on how many projects missed their deadline with P3 being 13% of the time late and standard projects being 25% of the time late. 45% of traditional projects exceeded their budgets on average by 35% while only 14% P3 projects did so by an average of 12%.

The answer whether P3 is an obvious solution to building infrastructure where there is not enough money in public budgets, also depends on whether one deals with money making infrastructure or money losing infrastructure. P3 on a money generator (a toll road) is a very different animal than a P3 on a money losing proposition like transit or a non-toll roadway.

In transit proceeds from operation are usually only in the 30% range of cost, sometimes a bit more, sometimes less. While a travel plaza or the Port of Baltimore (the two Maryland P3 precedents) can easily exceed operational cost and be used for the payback and profit to the private partner, transit fares will never generate enough money to pay operations and pay-back.

In those situations the public has to offer hard cash in from of "mortgage" payments (availability payments) taken from other sources or the general fund. And those payments may increase if projections about the revenue generation from the project itself don't realize as anticipated. Revenue projections are only one of the many variables that can create surprises during the life-time of a P3 project.

In any type of project there is an interesting relation between initial cost and operating cost, a relation that is typically inverse proportional, i.e. lower operating cost means higher initial cost and vice versa. In a standard design-bid-build model public works project the private side deals with the initial cost and the public side with operations. In a design-build-and operate model the private side deals with both sides of the equation. This has the potential to balance the conflict out, especially if the operating time in the P3 contract is long enough. Still, it is hard avoid the possibility that the private side will hand the project back to the public at the very moment when everything falls apart, because either too much had been cut out of initial cost (a risk the private side could take if the operating period was short) or the private side deferred maintenance knowing when it could return the project.

Proponents of the P3 model generally emphasize that the private participation in construction, operation and management is not to be equated with privatization since the assets themselves remain in private hand. In the case of the Maryland Purple Line, the State would own the entire asset after 36 years, comparable to a lease buy model.

However, it is only logical to expand from construction and management of new facilities to considering a transfer of already existing facilities and turn operations and management for those to the private side. Full privatization through sale is then the just last and final step. All models have been tried for a variety of public assets and services from municipal waste collection to municipal water and even parking meter operation.

Privatization of public assets under a lease model is a tricky business. While efficiencies can be had with this route, it is a question who gets the benefits and who gets the risks, the public or the private side. Very lucrative assets such as on-street meter parking or parking garages may pay big sums to a municipality at the time of sale but the public loses a reliable long-term funding stream. Ultimately such a sale could mean that it makes the private sector rich while municipalities are poorer than before. Selling assets in this way is like Sears trying to avoid bankruptcy by selling the Craftsman tool brand. It provides momentary liquidity but further dims the prospect of a recovery of the ailing corporation. In the case of public works, the provider of transit, water, or electricity has an almost complete monopoly over the service because the infrastructure needed to provided it exists only once. It is rare to have duplicate water, electric or rail lines with competing services. The monopoly needs to be tightly regulated to balance public interest with the private profit motive. In some cases the response to the monopoly issue has been to allow competing services on one and the same infrastructure, for example, competing train operators on the same tracks (a practice common in England, Germany) or electricity providers using the same distribution network (common in the US).

|

| Denver Eagle P3 at the Denver International Airport |

Even the transfer of assets which produce little or no income is able to undermine the fiscal stability of a public agency through extended availability payments. The likelihood is that risks become socialized and profits privatized.

One of the more painful ways for the public to pay is through increased user fees or rates for transit rides, utilities or parking. Many cities and their residents have had terrible experiences with privatized utilities, waterworks, transit services or private entities running parking meters. In many cases service didn't become better and fees went through the roof.

On the other hand, if there is sufficient value creation, ideally in areas adjacent to the project, where the private side cannot collect all the benefits (such as added property values, i.e. taxes along a transit corridor) the hardship of payback and added total cost can be mitigated through those increased revenues. In other words, when the prospect of infrastructure investment rescues an area or jurisdiction from a spiral of decline and decreasing revenues and the added value leads to a virtuous cycle of increased revenues, having leveraged the game changer through a P3, mortgaging the future may have well been worth it.

A classic case of that model is transit oriented development. Whether private or public entities build and manage transit and real estate, a virtuous cycle of value capture is possible in which cost and revenue are brought into balance by a broader approach to revenue creation. In fact, the only transit agencies in the world which operate transit with black numbers do so because they also have large real estate holdings. (Singapore, Hongkong). Value capture, of course, does not require a P3, its benefits can be accrued in any of the project delivery configurations discussed above.

P3 is not the magic bullet that will solve all of the US infrastructure woes. It will play a role in getting major projects started in an era with little public appetite for taxes and fees. In the end, though, there is no such thing as a free bridge, as Hunter Blair put it, and no way around the fact that infrastructure will be only as good as the public is willing to pay for it, in one way or another.

Klaus Philipsen, FAIA

FHWA P3 Toolkit

The Perils of P3

Remember: Public-Private Partnerships Aren't Free. (CityLab)

No Free Bridge, Economic Policy Institute 2017

Maryland approves $5.6 billion Purple Line contract (Washington Post)

Taxpayers vs. Private Investors: Shifting the Risk of Funding Public Projects (NEXT City)

No comments:

Post a Comment